Blogs

Read our latest news and industry insights.

Investment Management

We remain positive on the South African equity market and the renewed positive sentiment driven by resilient earnings and political reform. The JSE (Johannesburg Stock Exchange) however, constitutes less than 1% of global stock markets. If your portfolio only consists of South African assets, your overall portfolio risk may be concentrated in region specific factors. You may also run the risk of losing out on opportunities not offered by local markets. As we head towards the final quarter of the year, this may also serve as a reminder that your annual R1m discretionary allowance and the foreign capital allowance of up to R10m expires on 31 December 2024. It may also be a good time to capitalise on US Dollar weakness for long-term currency hedging. What should you be careful of when investing directly offshore? One of the risks in offshore investing is probate. Offshore probate refers to the process of applying for the right to deal with a deceased investor’s foreign assets and proving their will as a valid legal document in the foreign jurisdiction. The second risk is situs tax that will be encountered in both the US and UK. Situs tax refers to the taxation of assets based on their location or situs. In other words, it is the jurisdiction where the property is located, or deemed to be located, that determines the taxation of that property. What structures provide solutions? Structures where the foreign assets are held by a local nominee company. “Wrapped” structures like sinking funds or endowment policies. Estate planning benefits? It’s important to consider the estate planning benefits of using the correct structure. Normally structures that allow beneficiary nomination provides regulatory- and tax benefits. It can be useful in lowering estate related costs but also provide cash flow to beneficiaries before the estate is wound up. The above considerations may also not be applicable to certain investors. There are structures for those investors who have ceased or are ceasing to be South African tax residents. It may also be suitable for the investor’s adult children living abroad (non-SA tax resident). Estate duty or the equivalent may be payable in their country of residence. Ruvan J Grobler RFP™ (PGDip Financial Planning)

Liquidity Risk in your Investment Portfolio There is nothing worse than being in a pickle and you have no emergency funds. This is when people get into unnecessary debt with high-interest unsecured debt via credit cards and personal loans. To avoid this, you must plan your investment portfolio around long-term growth as well as liquidity needs. Setting financial goals in the financial planning process is an effective tool in providing a practical framework. But it also gives wealth managers possible investment horizons and importantly, the liquidity needs of a client. There is a tightrope to walk between providing liquidity and enjoying long-term growth and your age and specific needs will determine how far you lean towards each side. Here are some of the liquidity risks that you may face in your investment portfolio: Product Rules: Certain structures allow partial access to funds, and some offer no access to funds within a certain term. Examples: Compulsory investment products like pre- and post-retirement structures. Discretionary investment products like endowments, sinking funds and structured products. Asset Allocation: With short-term volatility in growth assets like equities you may run the risk of selling during a downturn, locking in losses. It’s important to rather consider the use of conservative interest-bearing assets when planning for short-term or emergency liquidity needs. Demand: All assets are not desirable by investors. An example can include private equity shares that may not be well known or desired. This will make it difficult to sell when funds are needed because there might not be a willing buyer. Availability: In certain instances, investor funds are pooled together in order to buy a large underlying asset. Some of these assets can have a maturity date attached leaving no room for buy-backs before maturity. How can you assess the need with asset allocation in mind? High liquidity – Conservative allocation – Low volatility Low liquidity – Aggressive allocation – High volatility *This is not financial advice. Ruvan J Grobler RFP™ (PGDip Financial Planning)

Investment fees should not be difficult to understand and must at all times be transparent. Many years ago, this was not the case but in recent years the industry has standardized the terms and set out clear limits.

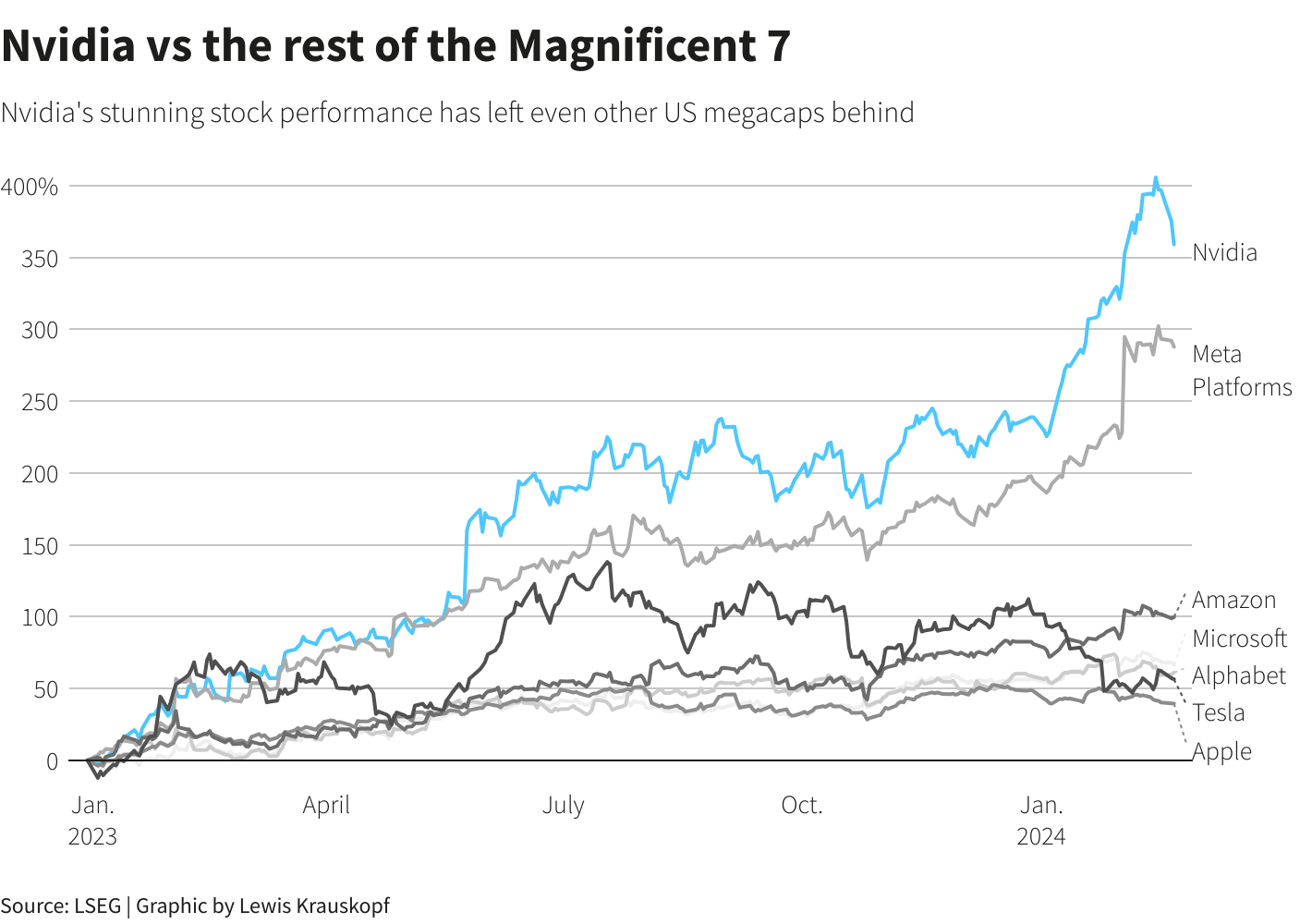

"Shares like Nvidia can form part of a well-diversified investment portfolio where market risk is managed."